The other day, I wrote an article introducing the pension system in the United States and the types of related accounts, but this time I would like to introduce investment funds that are listed as one of the investment destinations when actually investing the money you have contributed.

What Is an Investment Fund?

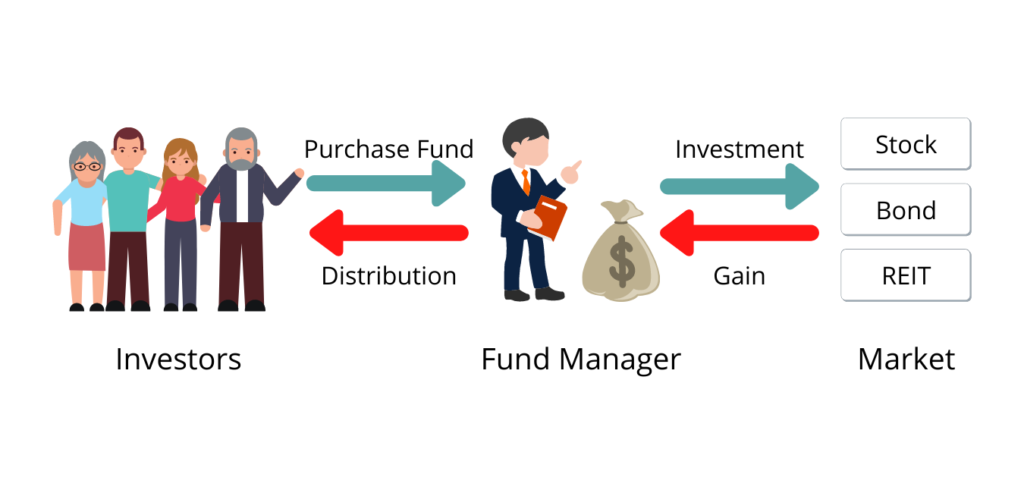

Investment funds are financial instruments in which money collected from investors is aggregated as one large fund, and a fund manager invests it in stocks and bonds, etc. and distributes its profits to investors.

In a regular stock investment, “buy one product” = “buy one stock”, but since multiple stocks are combined in one product in an investment fund, it can make enable the investors to invest in various assets just by purchasing one product.

Fund managers distribute funds collected from investors in bonds, stocks, real estate, etc., both domestically and internationally.

Investors can choose between the fund manager to entrust the management and the amount to invest, but since the management itself is left to the fund manager, it is possible to manage the asset without specialized investment knowledge.

Since the investment destination of the collected funds varies depending on the investment trust that the investor purchases, it is necessary to carefully select products in order to reduce investment risk.

Since the operating results of investment funds vary depending on the market environment, after purchasing an investment fund, the investment fund may be well operated and profitable, or it may be poorly operated and lose less than the amount invested.

Therefore, since all profits and losses from a result of the investment fund’s performance belong to investors according to their respective investment amounts, investment funds are not financial instruments for which the principal is guaranteed like a regular checking and saving bank accounts.

In addition, specifically speaking, the main investment funds in Japan are translated as Investment Trusts, and the main investment funds in the United States are the Mutual Fund, so their governances and systems are slightly different; however, this article introduces them collectively as investment funds.

Investment Trust

When it’s called Japanese investment funds, most of them are investment trusts which is also called a contract-type investment fund.

A contract-type investment fund is a fund in which three parties contract to manage assets: a fund manager, a custodian, and an investor.

There is a distributor as an intermediary for investors, and only the distributor owns the investor’s information.

Mutual Fund

On the other hand, the main investment funds in the United States is the mutual fund.

It is a form of investment vehicle made up of of a pool money collected from many investors to invest in securities like stocks and bonds. In the mutual fund, each investor entrusts the fund manager to invest the funds for various securities.

Investment gains are returned as dividends to investors who have shares.

Since shareholders have voting rights at the general meeting of shareholders, and they can exercise their voting rights on important management matters, such as the appointment and dismissal of executive officers, audit officers, and accounting auditors of mutual fund.

How Investment Funds Work

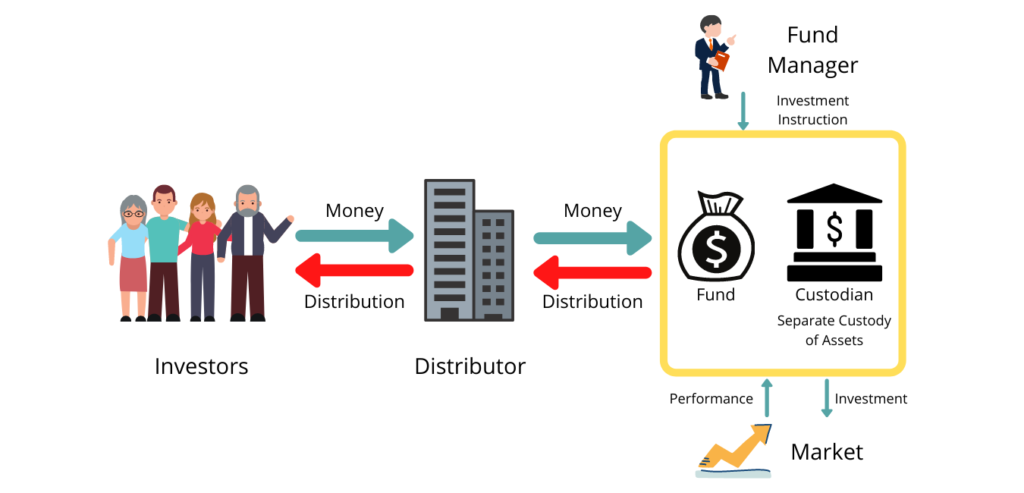

Investment funds in Japan are made by “fund manager” and sold through “distributors” such as securities companies and banks.

The distributor sells investment funds to investors, and the investor deposits funds with the distributor.

Funds collected from investors are collected together and stored in a “custodian” specializing in asset management from the distributor.

The fund manager instructs the custodian where and how much to invest the money in the market.

The custodian buys and sells stocks and bonds under the direction of the fund manager.

Custodian stores and manages money, but the management authority for the funds is solely with the fund manager, and custodians cannot buy or sell stocks or bonds without the direction of the fund manager.

When the results of the investment are obtained, the custodian will give distributions and redemptions to the distributor, and the proceeds will be distributed to each investor.

In this way, investment funds are financial instruments in which each individual specialized institution plays a its own role. The fund managers are responsible for investing and managing funds, distributors are bridges between investors and fund managers, and custodians undertake the management of funds. Thus, it allows investors to invest their money safely and securely.

The structure of investment funds in the U.S. is slightly different from Japan, such as whether investors have voting rights, but from an investor’s point of view, it is roughly the same.

Benefits of Investment Fund

There are five advantages of investment funds:

- Invest from a small amount

- Reduce risk with a diversified portfolio

- Be entrusted with the operation by an investment professional

- Invest in countries, regions, and assets that are difficult for individuals to invest in

- Highly transparent and reliable to invest in

- Safety

Invest from a small amount

Usually, individual stock investments and bond investments require a large amount of money, but with investment fund, investors can easily make their investment with much smaller amounts.

Reduce risk with a diversified investment

As there is a famous proverb “Don’t put all your eggs in one basket”, in asset management, in order to reduce the investment risk as much as possible, there is an idea that it is better to invest in multiple products instead of investing only in a specific product.

While individual investors need a lot of money in order to make diversified portfolio if they invest their money into each company by themselves, investment funds collect small amounts of money from many investors and manage them as one large fund, allowing them to invest in a variety of assets and reduce risk.

Be entrusted with the operation by an investment professional

It is very difficult for individuals to acquire the knowledge and methods necessary for investing in stocks and bonds.

Investment funds are operated on behalf of investors by experts who have knowledge of the economy and finance, obtaining and analyzing various information, such as economic and economic movements, and corporate performance.

In addition, even for individual investors who are busy with work or private life and do not have time to check investment information frequently, investment funds can leave management to experts, so it is convenient in that respect.

Invest in countries, regions, and assets that are difficult for individuals to invest in

Investment funds can also invest in overseas stocks, bonds, and special financial products that are difficult to buy or sometime not available for individuals investors.

Highly transparent and reliable to invest in

In principle, investment funds have a net asset value that is the daily transaction price, and it is a financial instrument that is easy to understand asset value and price movement.

In addition, since each financial result is audited by an audit firm, etc., it can be said that transparency is also high.

Safety

As I mentioned earlier, investment funds are financial instruments that can be made up of each institution, such as distributors, fund managers, and custodians, playing their respective roles.

Under the structure of investment funds, even if each institution involved in investment funds goes bankrupt, the money deposited by investors is institutionally protected regardless of the amount of investment.

For example, even if a distributor goes bankrupt, investors’ money is managed by the custodian as trust property, so trust property is not affected.

In addition, since the fund manager does not store or manage trust property only by making management instructions, even if the fund manager goes bankrupt, the trust assets are stored in the custodian, so there is no direct impact on the trust property.

Custodian that were under management will be carried over to other fund manager or the fund will be redeemed.

Finally, you might be worried about what will happen if the custodian goes bankrupt, but since it is required by law that trust property is managed separately from the custodian’s own property, there is no impact on trust property even if the custodian goes bankrupt.

If the custodian goes bankrupt, an investment fund is canceled and returned at the value at the time of failure, or if the trust property is transferred to another custodian, the investor can hold the investment fund as it is.

In this way, investment fund is a system in which investors’ trust assets are protected even if each specialized institution fails.

Disadvantages of Investment Funds

The disadvantages of investment funds are as follows:

No original principal is guaranteed

Unlike savings, investment funds do not guarantee the original principal amount, so be careful.

Investment funds may sell less than the purchase amount if their investment results do not improve and the price drops from the time of purchase.

Various High Cost

Since investment funds are managed by professionals to make investments, it is necessary to pay expenses to the professionals who operates them.

Costs vary by fund, but mainly include:

- Purchase commission: Fees required to purchase investment funds

- Fund management costs: Expenses for investment fund management

- Redemption fee: The cost of selling securities when a investment fund is redeemed

Risks of Investment Funds

So, you know the advantages and disadvantages of investment funds now, but like other financial instruments, investment funds also have price movements due to stock market trends.

The main factors affecting the value of investment funds include:

Risk of price fluctuations

The possibility that the price of stocks and bonds incorporated by investment funds may fluctuate.

Stock prices are ultimately determined by market supply and demand, but risks arise from stock market fluctuations due to changes in domestic and overseas political and economic conditions, changes in economic outlooks, and corporate performance.

Risk of exchange rate fluctuations

There is a risk that the price of foreign currency-denominated assets will fluctuate due to fluctuations in foreign exchange rates.

In general, if you are investing in yen, if the yen appreciates, there is a negative impact, and if the yen weakens, there is a positive impact.

Investment funds that are operated in foreign stocks and bonds basically have a risk of currency fluctuations.

Default risk

There is a risk that the value of securities such as stocks and bonds will fall if interest and redemptions cannot be paid under predetermined conditions when financial and business performance deteriorates or management slumps.

Risk of interest rate fluctuations

There is a risk that the price of bonds will fluctuate when interest rates fluctuate due to fluctuations in policy interest rates.

In general, bond prices fall when interest rates go up, and bond prices go up when interest rates fall.

In addition, bonds with a long period of time to full term are greatly affected by interest rate fluctuations.

Country Risk

This is the risk of asset values fluctuating due to instability in the political, economic, social, international relations, etc. of the country (region) to which you are investing.

Liquidity risk

There is a risk that assets that cannot be traded under sufficient liquidity due to market size, trading volume, trading regulations, etc.

コメント